Carbon markets have emerged as one of the most powerful mechanisms steering investment decisions.

The global shift away from fossil fuels toward low- or zero-carbon energy systems—is no longer a matter of policy ambition- but a market reality. As governments tighten emissions caps and companies rush to meet net-zero commitments, carbon markets have emerged as one of the most powerful mechanisms steering investment decisions.

Whether through compliance systems like the EU Emissions Trading System (EU ETS) and China’s national carbon market, or through voluntary carbon credits that support renewable energy and carbon removal projects, carbon pricing is rewriting the economics of energy.

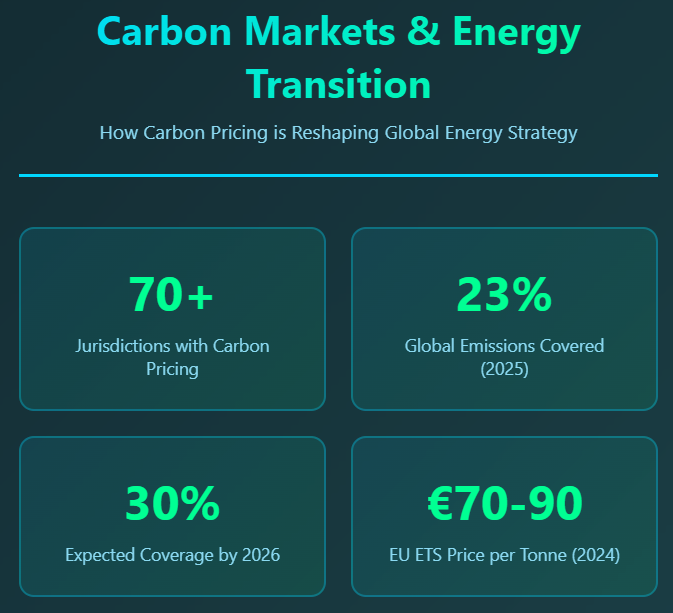

In 2025, more than 70 jurisdictions now implement some form of carbon pricing, covering roughly 23% of global greenhouse gas emissions. By 2026, that share is expected to exceed 30%, as carbon markets expand and link across regions. The message is clear: the cost of carbon is now a key input in the global energy equation.

Carbon markets convert climate policy into economic signals that influence corporate and investor behavior. By putting a tangible price on carbon pollution, these systems make fossil-intensive operations more expensive and low-carbon alternatives more competitive.

For energy companies and heavy industry, these markets serve as a cost of doing business and a guide for capital allocation. The higher and more predictable the carbon price, the faster firms shift investments toward low-carbon technologies like solar, wind, green hydrogen, and carbon capture.

The backbone of the global carbon market remains the compliance sector, where emitters are legally required to hold allowances matching their emissions. The EU ETS is the largest and most mature example.

In 2024, reforms known as the “Fit for 55” package tightened the emissions cap by 4.3% per year and expanded coverage to maritime transport and new industrial sectors. This shift has:

China’s compliance market, while less transparent, is poised for rapid expansion. The government plans to include aluminum, steel, and cement sectors by 2026, transforming its market into the largest by emissions coverage.

Meanwhile, emerging systems in Indonesia, South Korea, and Canada are integrating carbon pricing into national energy planning, aligning market incentives with decarbonization pathways.

Prediction: By 2026, nearly all G20 nations will have either a carbon tax, an emissions trading scheme, or linked offset markets influencing their national energy strategies.

Beyond compliance markets, the voluntary carbon market (VCM) allows companies to purchase carbon credits to offset residual emissions or support climate-positive projects. While controversial at times, the VCM is an important bridge for sectors that cannot yet fully decarbonize—particularly aviation, shipping, and oil and gas.

Renewable energy projects in developing countries once dominated voluntary markets, but as many grids have grown cleaner, the focus has shifted to nature-based and carbon removal projects. Yet, voluntary credits still play a role in supporting early-stage clean energy in emerging markets where grid emission factors remain high.

For instance, voluntary carbon finance has been instrumental in:

As companies transition from offsets to insets (reductions within their own value chains), voluntary carbon markets serve as testing grounds for new decarbonization models that can later inform national policy and regulation.

For corporations, carbon markets are no longer peripheral—they are integral to financial planning and disclosure. The Task Force on Climate-Related Financial Disclosures (TCFD) and International Sustainability Standards Board (ISSB) frameworks require companies to account for carbon pricing exposure.

Energy-intensive firms—utilities, cement producers, steelmakers—are now hedging carbon price risks just as they hedge fuel or currency exposure. Carbon allowances have become tradable assets, influencing share valuations and credit ratings.

Investors, too, are watching carbon exposure closely. Climate-aligned funds are favoring companies with:

For example, European utilities that rapidly adapted to high carbon prices by retiring coal and investing in renewables (such as Ørsted and Enel) have seen stock outperformance compared to lagging fossil-heavy peers.

In short, carbon markets are now a proxy for climate competitiveness.

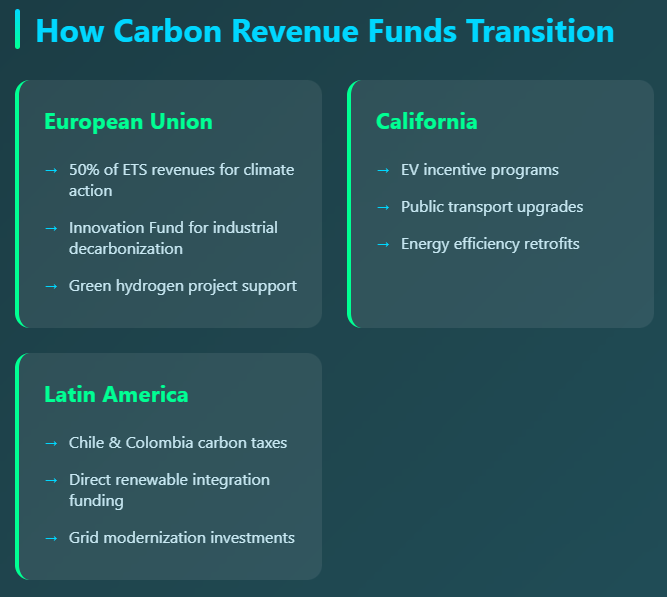

Carbon pricing doesn’t only penalize emissions—it funds the transition. Governments are increasingly recycling auction revenues and offset proceeds into clean energy projects.

As these mechanisms mature, carbon pricing revenue becomes a steady funding source for transition infrastructure—reducing reliance on public debt or subsidies. By 2026, it is expected that global carbon markets could mobilize over $100 billion annually for clean energy investments.

Technological innovation is transforming how carbon markets interact with energy systems. Digital MRV (Monitoring, Reporting, and Verification) platforms, satellite tracking, and blockchain registries now ensure higher transparency in emissions accounting.

For energy companies, these tools mean better integration of real-time carbon intensity data into operations and trading. For example:

This convergence of digital carbon infrastructure and energy analytics will make decarbonization more measurable, traceable, and investible—key to scaling private capital participation.

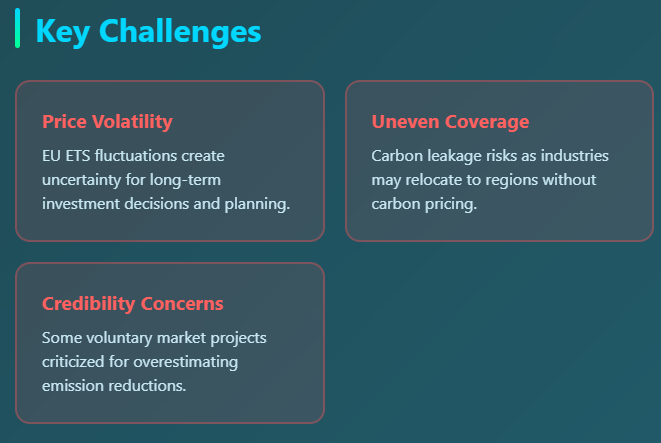

Despite progress, carbon markets face structural challenges that could slow their impact on the energy transition:

The solution lies in harmonization and linkage: aligning standards across borders and connecting systems to stabilize prices and improve liquidity. Initiatives under Article 6 of the Paris Agreement aim to create a more unified carbon accounting framework by 2026.

The global energy transition is accelerating, and carbon markets are no longer side mechanisms—they are central to how it happens. By internalizing the cost of emissions, they reward clean innovation, discipline polluters, and finance the infrastructure of a net-zero world.

As we move toward 2026, the most successful energy strategies will treat carbon markets not as compliance burdens but as investment opportunities—a chance to align profit with planetary stability.

treating them as investment opportunities rather than compliance burdens aligns profit with planetary stability.