In 2025, tools that once seemed futuristic (autonomous report generation, real-time policy intelligence, predictive price modeling) are now being adopted as standard in serious climate finance firms, consultancies, and registries.

Carbon credit markets have advanced into the stage that they are no longer just about offsets and allowances changing hands bilaterally. As a matter of fact, over the past few years, derivatives tied to carbon—futures, options, and exchange-cleared contracts—have scaled dramatically. Exchanges and trading houses are building infrastructure that turns carbon into a tradeable, hedgable, and investable commodity. That shift opens new capital and liquidity to finance decarbonization, but it also raises a hard question: is this healthy financialization that deepens the market, or a speculative layer that distorts climate outcomes?

This article explains how carbon derivatives have emerged, why institutional players are piling in, the benefits and pitfalls of financialization, and what market participants should watch in 2025 and even beyond into 2026.

A carbon derivative is a financial contract whose value is linked to the price of a carbon instrument-typically allowances from compliance systems (like EUAs) or standardized voluntary credits. Derivatives include futures (agreements to buy/sell at a future price), options (rights to buy/sell), and swaps. They let market participants hedge price risk, speculate on future allowance scarcity, or lock in prices for budgeting and project financing.

Derivatives matter because they introduce liquidity, enable price discovery, and allow large buyers (utilities, airlines, corporates) and traders to manage exposure. They also create standardized instruments that institutional investors and banks can underwrite and trade on regulated venues—bringing scale to what was once fragmented and opaque.

National Value of environmental futures & options tradded in 2024

20.4 million contracts traded on ICE alone – 40% year-over-year

The pace of adoption is striking. Intercontinental Exchange (ICE) reported a record 20.4 million environmental futures and options contracts traded in 2024-about a 40% year-over-year increase and equivalent to more than $1 trillion in notional value. That surge signals both rising participation and growing reliance on exchange-cleared carbon tools.

Major derivatives venues are also expanding product sets. In October 2024 the CME Group launched futures on Australian Carbon Credit Units (ACCUs) via its CBL partnership, enabling block trades and cleared positions tied to standardized voluntary credits. The launch was followed by initial block trades, demonstrating market appetite.

Meanwhile, futures and options on compliance allowances—most notably EU Allowances (EUAs)—have become core trading instruments on EEX, ICE and CME, with open interest and volumes rising as EU policy tightened caps and broadened sectors covered. Exchanges regularly publish high volumes and growing open interest, underscoring the institutionalization of carbon as an asset.

Finally, regulators are waking up. U.S. oversight bodies signaled new guidance in 2024–25 to strengthen rules around carbon-related derivatives and the underlying credits—aimed at preventing fraud, improving transparency, and protecting markets. That regulatory attention reflects carbon derivatives’ growing systemic importance.

Collectively, these forces can help transform tiny, fragmented carbon markets into robust financial markets that channel capital into verified emissions reductions-if integrity is protected.

Brands must avoid overclaiming. The most effective messaging:

The good news: both market participants and regulators are already responding. Exchanges and custodians are building delivery and settlement systems tied to vetted registries; platforms like CBL/Xpansiv are integrating registry data to improve deliverability and traceability of offset-backed contracts.

Regulators-at least in some jurisdictions-are adding targeted oversight. The U.S. moved to clarify guidance on carbon derivatives and the integrity of offsets used in financial instruments, while EU reforms keep tightening cap schedules and compliance rules that underpin allowance prices. These interventions aim to retain the benefits of liquidity while limiting manipulation and low-quality credit proliferation.

Meanwhile, private initiatives-rating agencies for credit quality, industry codes (ICVCM/VCMI), and data providers-are emerging to rate and screen credits, improving the inputs that feed derivative markets. Buyers increasingly demand CCP-aligned or high-integrity credits for settlement and delivery, raising the bar for tradable inventory.

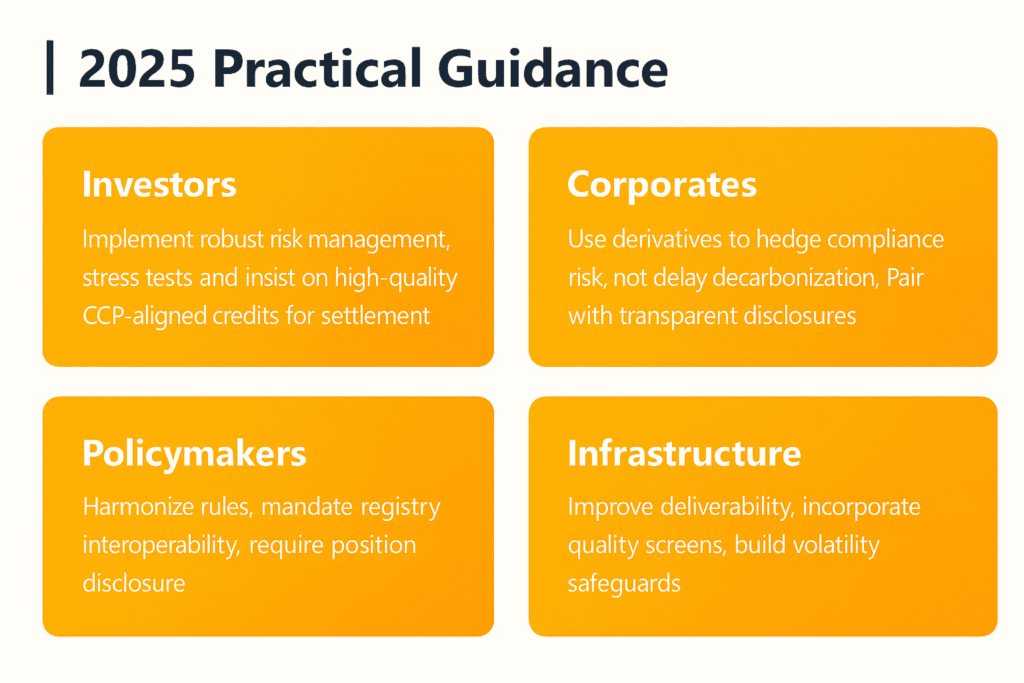

Practical advice for investors, corporates and policymakers (2025)

Carbon derivatives represent real progress when they bring liquidity, transparent price signals, and financing to decarbonization. But financialization without strong integrity safeguards risks turning climate instruments into speculative assets that undermine environmental goals.

The path forward is conditional: keep building scalable, cleared markets—while enforcing quality, transparency, and alignment with climate policy. If market design, regulation, and verification improve in step with trading innovation, derivatives can be a tool for progress rather than a distraction from it.

Carbon derivatives represent conditional progress – they can channel

capital to decorbonization If paired with strong integrity safeguards,

quality standards, and aligned climate policy