Latin America contains some of the world’s richest natural carbon sinks: vast tropical forests, peatlands, mangroves, and productive grasslands that together store billions of tonnes of CO₂.

Latin America contains some of the world’s richest natural carbon sinks: vast tropical forests, peatlands, mangroves, and productive grasslands that together store billions of tonnes of CO₂. As companies and governments seek high-integrity nature-based carbon credits, the region’s bio-diverse landscapes and relatively low per-ton sequestration costs make it a logical supply hub. But unlocking that potential at scale requires navigating governance, social safeguards, and measurement hurdles—and recent developments show both progress and cautionary signs.

Three features make Latin America uniquely important for nature-based carbon supply:

These factors explain why private and public buyers have begun signing large deals and why governments are crafting market frameworks that aim to capture greater domestic value.

The past two years have seen headline transactions and pilot programs that demonstrate both private demand and government willingness to transact at scale. For example, Amazon state-level deals backed by the LEAF Coalition signaled major corporate interest and public-private ambition for jurisdictional credits.

Brazilian states have also moved to monetize forest outcomes: Tocantins announced a major program to offer tens of millions of credits through 2030, and global tech firms have purchased nature-based removals from Brazilian restoration projects—moves that reveal appetite for high-quality, locally generated credits.

More recently, banks and financiers have begun structuring deals: partnerships between subnational governments and global banks (for example, agreements to sell jurisdictional forest credits) illustrate how capital markets can be marshaled for forest protection while embedding community benefit provisions. These developments show supply is being organized, not just produced project-by-project.

When structured with robust governance and community participation, these pathways can transform latent ecological capital into durable finance for conservation and livelihoods.

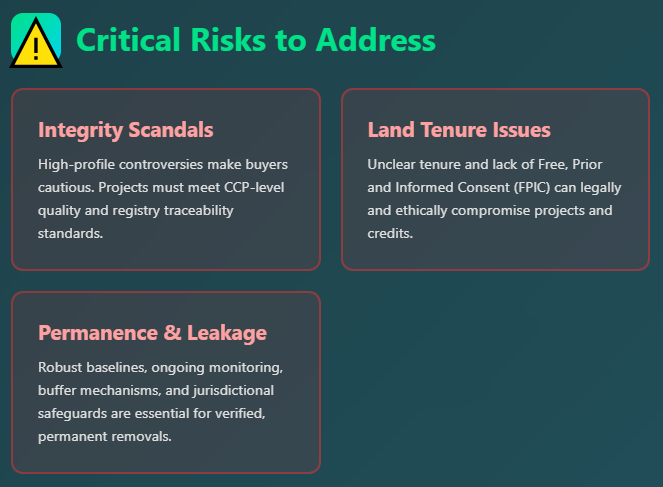

Despite potential, Latin America faces three practical obstacles that can limit growth or provoke buyer backlash if not addressed:

If these risks are mishandled, buyers may avoid the region or pay discounts, undermining the potential economic upside.

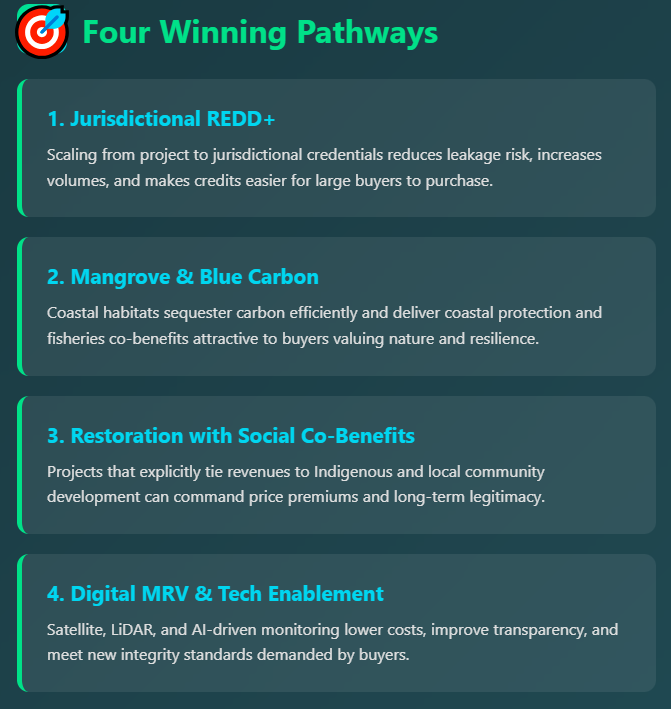

To translate ecological potential into marketable credits, stakeholders across Latin America should prioritize:

Where these elements are present, projects tend to attract higher prices and more secure offtake agreements. Recent deals that emphasize community shares and robust vetting are already examples buyers cite as models.

Based on recent trajectories and buyer signals, here’s a concise, evidence-based forecast for 2026:

If these conditions are met, Latin America could significantly expand its share of the high-integrity voluntary market by 2026—and attract new long-term capital to conservation and restoration.

Latin America’s natural capital offers one of the fastest routes to scale nature-based climate finance. But scale without integrity will be self-defeating. The region’s future in carbon markets depends on marrying ambition with accountability: jurisdictional deals, secure community rights, transparent registries, and tech-backed MRV. For buyers and investors willing to engage patiently and ethically, Latin America could supply large volumes of high-integrity credits—and deliver tangible development co-benefits—by 2026.